Beyond Arbitrage: DATs as the Corporate Wrappers for On-Chain Capital Markets

It’s 2025. Real returns are nowhere to be found. Large asset managers are turning towards crypto but need a way to safely tap its upside potential. Could DATs be the key to unlocking on-chain value?

By Arpan Bagui from Republic Technologies

Helpful Terminology:

DATs = Digital Asset Treasury Companies - public companies that accumulate crypto on a balance sheet and use capital markets to buy more

mNAV = market cap / net asset value (book)

On-chain yield = staking/DeFi yield from ETH or other assets.

BTC yield = % change in BTC-per-share from accretive issuance/financing (not staking)

Galaxy released an article in late July titled The Rise of Digital Asset Treasury Companies. It’s a good primer on the DAT business model and helpful background for anyone curious. It also shows how much more sophisticated Galaxy’s viewpoint on DATs has become since May when they compared DATs to dotcom bust startups1.

Of course healthy skepticism around DATs is well-warranted and seems to have approached a relative high. Humorous and insightful Bloomberg columnist Matt Levine has a famous extended analogy comparing crypto to magic beans. He says DATs take $1 of those magic beans, put them in a box, and sell them on the stock market for $2, using the proceeds to buy more magic beans. It’s a light-hearted comparison that shines a critical light on the DAT business model. It also captures the essence of the mainstream opinion on DATs: they are an arbitrage trade, not financial innovation. As this trade gets crowded, premiums will fall and the entire flywheel falls apart. This seems to be the consensus, anyway, and as mNAVs have compressed many are wondering how much longer these DATs stick around.

“It looks a little bit like crypto keeps playing a prank on the stock market, and the stock market keeps falling for it.”

- Matt Levine, Bloomberg Columnist in April 2025

Below I make the case that DATs are not pranks. DATs are very distinct from the speculative bubbles that created the ICOs of 2017, the SPACs of 2020, the NFT rugpulls of 2022, etc. because DATs are necessary to blockchain adoption. Specifically, they solve the access-to-crypto problem which is a major issue facing large asset allocators.

In other words, $1 of crypto on a balance sheet is indeed worth more than $1 of crypto otherwise.

The search for real returns

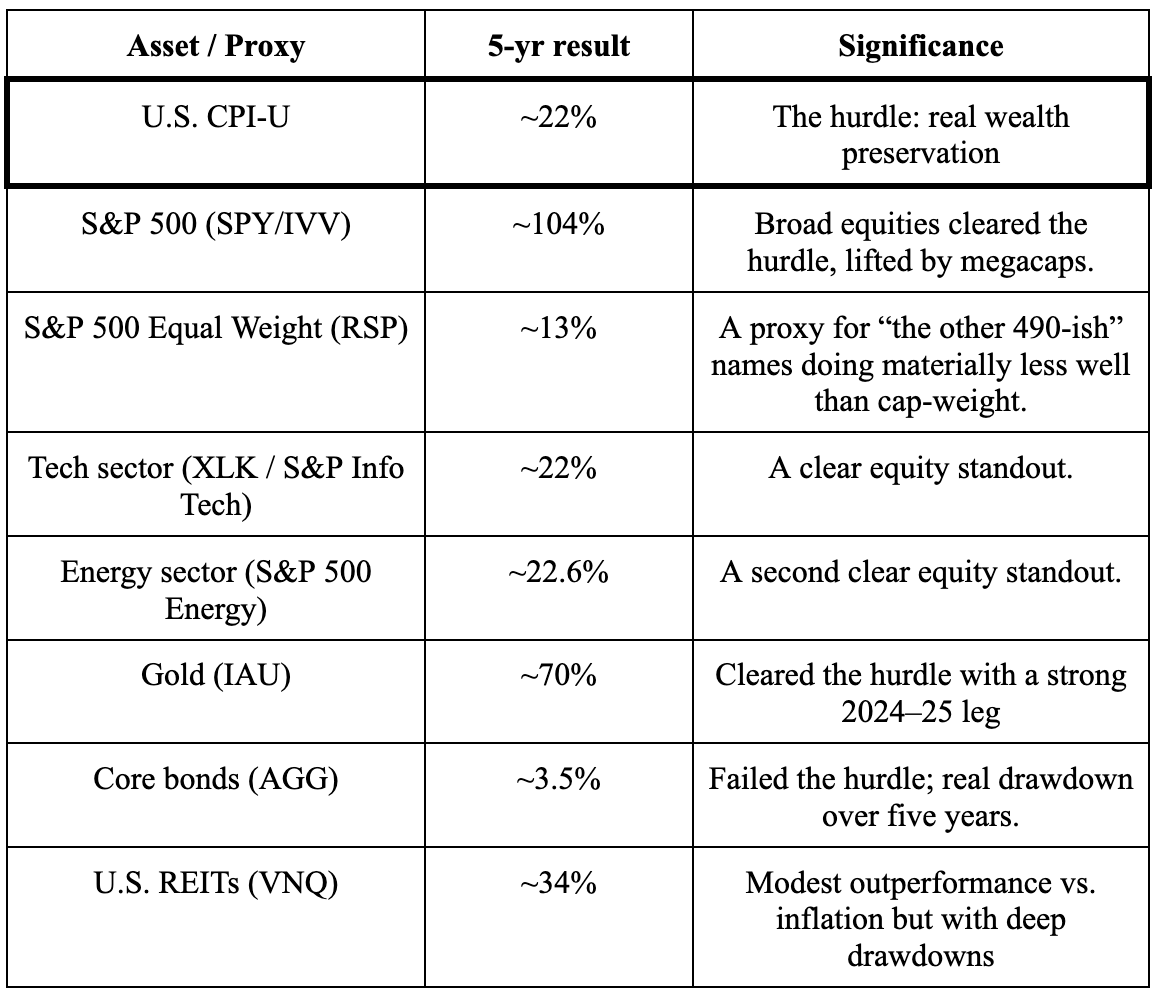

Let’s start at the top with macro (stock market macro, at least). The market has been doing well, the S&P 500 is up over 100% cumulatively over the past 5-years. But top-line nominal returns across asset classes hide the fact that only a few sectors are actually beating inflation. Over the last five years the price level rose ~22% (or ~4-5% annualized in CPI terms). In other words, for wealth to tread water in real terms returns have had to clear a ~ 4-5% annualized hurdle, ~20% cumulative, over that period.2

Across the big buckets, only a handful of asset classes consistently cleared that hurdle.

This is the tale of two markets that has been well-documented by market analysts and economists. Compare the second and third rows in the table above. The S&P500 is primarily being lifted by large tech stocks. In 2021, analysts were already warning that the S&P’s top handful of names had approached record weights; by mid-2025, the top ten were again near record share of market cap, with Nvidia alone roughly 8% of the index.

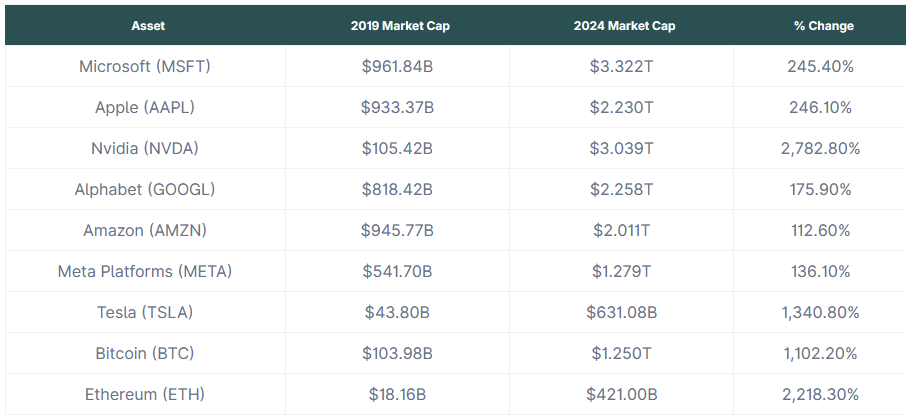

However, there is another asset class with outstanding real returns: crypto. In late 2024, BlackRock compared BTC to the Magnificent-73 and in fact BTC and ETH have both outperformed most of the Mag-7 over the past 5 years. The center of gravity for upside has started to shift on-chain4.

Why is this happening?

BTC and ETH are gaining value for a lot of reasons. The most timely and relevant reason is discussed below.

The global financial infrastructure is going through an upgrade. The clunky Rube Goldberg machine of banks/processors/merchants handing messages back and forth is being gradually replaced by blockchains. Blockchains enable 24/7 rails and programmable money which are necessary for a truly digital economy.

Two recent catalysts that have accelerated the pace of blockchain adoption:

Regulatory clarity for access products. U.S. spot ETH listing approvals in May 2024 removed legal uncertainty on top of January’s spot BTC ETFs, in other words, price-exposure wrappers now exist inside the U.S. securities regime5.

A federal stablecoin framework. The GENIUS Act (July 2025) created the first federal regime for payment stablecoins. Issuers now have a path, reserve rules, and disclosure standards. As dollar-backed stablecoins scale, they pull activity on-chain and help ETH accrue value via demand for blockspace/settlement while BTC continues to establish itself as an on-chain store of value.

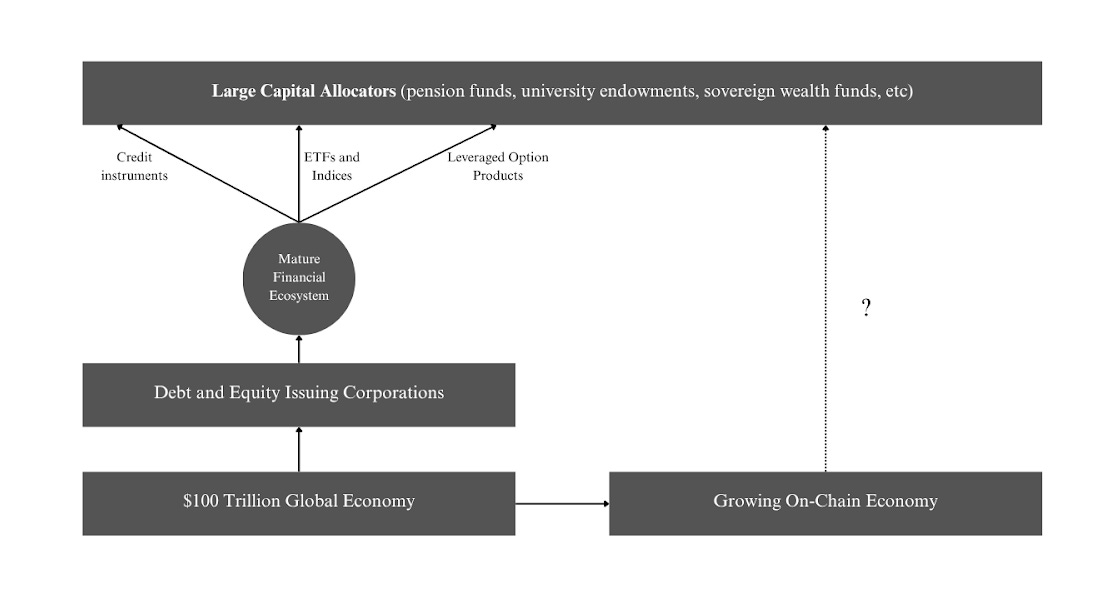

Roughly speaking, as blockchain adoption increases value accrues to BTC and ETH. This is key; return is increasingly embedded in assets (BTC/ETH) rather than operating companies. The old financial plumbing was not built for this. In the corporate world, it’s easy to build indices, credit ladders, and options structures on top of a company’s equity/debt. In crypto, the underlying upside sits in non-corporate assets. Thus, the access-to-crypto problem:

The group of massive asset managers who allocate the majority of global wealth – pensions, endowments, insurers, and sovereign wealth funds – have been fleeing towards the “frontiers of return”. But now since that frontier exists outside of corporate balance sheets, large asset managers have no way to access it. For a sense of scale on how much capital this actually is:

Pensions: ~$63T6 +

Insurers: $40–42T7 +

Sovereign wealth funds: ~$14T8 +

U.S. higher-ed endowments: $874B9 +

Total = ~$100T

This >$100T aggregate group of asset managers represents most of the $115T global economy, and they all pretty much invest the same way. Their investment mandate is characterized by long-horizons, and conservative investment approaches that anchor global savings and set the tone for markets and funding conditions. When this cohort rotates, entire asset classes reprice.

In a world where the inflation hurdle continues to shift up, protecting client wealth forces allocators toward assets that can clear it. So the problem becomes “how does global wealth, the majority of the global economy, keep up with real returns if they exist mostly on-chain?”

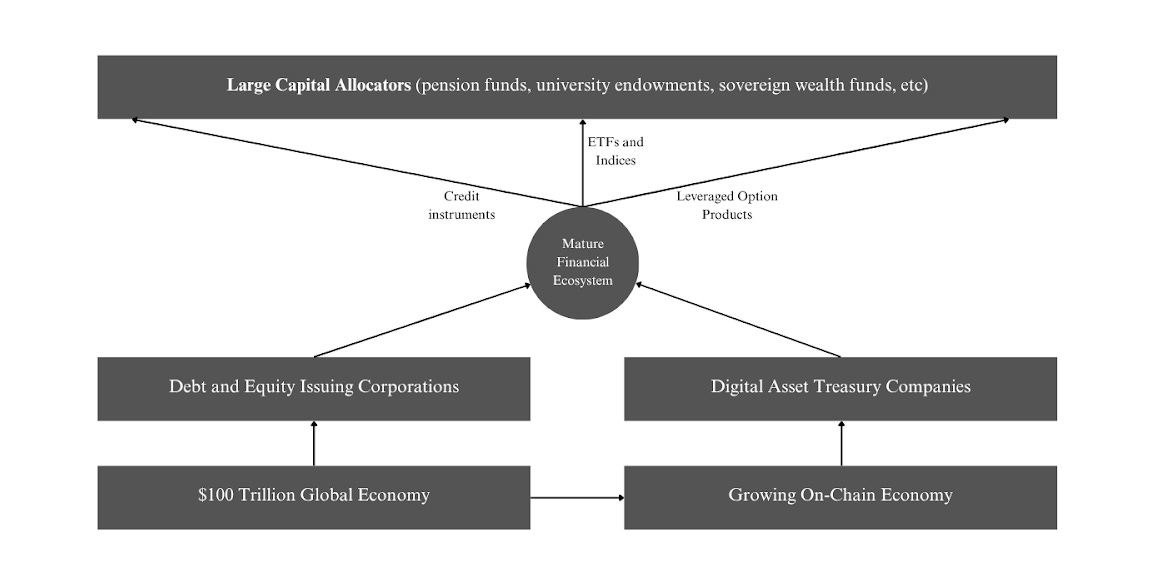

This is the problem DATs solve. A DAT represents the familiar corporate wrapper that holds BTC/ETH on balance sheet, raises equity and/or credit against it, and becomes raw material for indices, credit baskets, structured notes, and hedging markets.

In summary:

The capital that moves the global economy (pensions, endowments, insurers, sovereign wealth funds) wants the on-chain upside because it has outpaced the traditional equity returns on multi-year windows. This is happening in a world where few asset classes generate the returns necessary to outpace inflation.

But they can’t own it the way retail or a hedge fund can. They need mandate-friendly, liquidity-aware, credit-stack-friendly wrappers.

ETFs only partially solve it. They provide price exposure but don’t unlock the full stack of instruments (credit, converts, structured notes, term financing) that allocators and dealers use to shape risk across a yield curve. We’ll discuss the deficiencies of ETFs further in the next section.

No ETFs aren’t enough; DATs are uniquely necessary for the economic shift on-chain

Accessing the upside of innovative market sectors is typically not a problem in the world of traditional finance. Our financial system has become proficient at taking in cash flows from corporations and turning them into a spectrum of financial products across the risk-return curve. However, this presupposes a corporate issuer with a balance sheet and a capital structure.

When it comes to the upside embedded in ETH and BTC, there is no operating company producing those cash flows, they are assets native to decentralized blockchains. This means there are no corporate balance sheets to build those products on top of. ETFs were a step forward: they plug into brokerage rails, provide price exposure, and enable listed options useful for hedging. That’s good. But ETFs are poorly suited for creating a capital stack on top of.

While ETFs may deliver price exposure and exchange-traded options, they do not have corporate balance sheets. They don’t issue debt, don’t underwrite convertibles, and don’t warehouse financing or liquidity risk the way an operating issuer can.

Most large allocators want exposures along a curve (short-duration credit, term notes, converts with upside, etc.). That stack is born from issuers and banks, not funds. The ETF wrapper is great for beta and hedging; it is not the foundation for primary capital markets activity.

Issuers with crypto on a balance sheet have far greater capacity to grow their treasury and generate yield for the shareholders of their common stock. Consequently, there’s more value flowing through to the capital stack built on top of that common stock.

DATs fulfill a clear role in plugging the gap, providing the necessary vehicle for the financial system to ingest crypto and turn it into a variety of financial products for large capital allocators. This represents a win-win-win:

The traditional financial ecosystem now has a familiar corporation wrapper on crypto to create financial instruments from and is more aligned with on-chain growth

Large capital allocators can gain access to the upside and protect against their downside through the various financial products built on top of DATs

DATs can continue growing their treasury and serve as liquid crypto wrappers for the traditional finance ecosystem to build on, leading the way for slow-moving yet large amounts of capital to be exposed to the on-chain economy.

Comparing DATs to high-growth tech stocks

High-growth tech stocks have represented most of the S&P’s growth over the past decade, but concentrated returns in this sector create idiosyncratic risk and large capital allocators are looking for new frontiers of real return.

DATs are similar to high-tech growth stocks from a risk-return profile since they can capture the price appreciation of BTC and ETH on a balance sheet. This solves the need capital allocators have for financial products that increase in value with cryptocurrencies. They also enable a key unlock for the on-chain economy, allowing a way for slow-moving but massive capital to become exposed to the upside on-chain. However, they differ from tech stocks in some key ways:

Cash flows vs. balance-sheet assets

Big tech develops and sells products that generate cash flows; for DATs the balance sheet is the product and more specifically the increasing asset-per-share over time that DATs deliver. If a big tech company reports less than savory earnings indicating a declining demand in their products, their share price falls. Similarly if a DAT is unable to create sustained asset-per-share (see BTC Yield in terminology section) growth over time, its share price (and as a result its mNAV) will also fall.

P/E vs mNAV as measures of premium

Many analysts have made a comparison between the P/E multiple on traditional equities and the mNAV multiple on DATs. Both represent a “premium” that the market is willing to pay for future growth. For tech stocks, that growth stems from cash flows. For DATs, that growth stems from an increase in asset per share. But the average forward P/E on the tech sector is around 40x right now and earnings growth has been slowing down. This suggests that the relatively higher upside source of real returns lies with DATs.

P/E vs mNAV, a crucial difference

P/E and mNAVs are distinct in the sense that while a tech company does not need high valuations (elevated P/E’s) to be successful, a DAT does need elevated mNAV’s to scale. Of course a DAT can survive for short periods of time with a mNAV < 1x (trading below book) for short periods of time as MSTR did in 2022, but in order to grow the treasury it needs to be able to raise at a premium to book so it can purchase progressively more crypto. This is one key difference between P/E and mNAVs, and the discrepancy arises because mNAVs are crucial to a DATs product, its balance sheet, whereas P/Es are (usually) not.

Functionally, then, if DATs fulfill the same role those equities fulfill for allocators, we would expect to see a similar kind of demand for them as we do for tech equities.

The best example of this can be seen with Strategy, which pivoted from its tech solutions business model to a Bitcoin treasury model in 2020. Today about 60% of MSTR’s public float is held by institutional capital (similar to/ a bit lower than large cap tech stocks), which uses MSTR common and its preferred/credit issuance as building blocks for larger indices, ETFs, and passive income funds10.

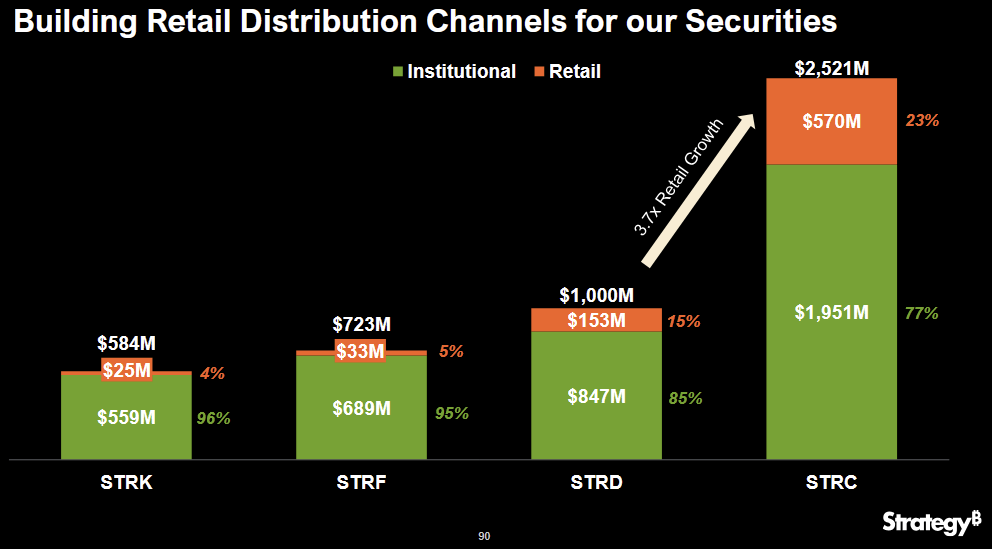

Additionally, being the most mature DAT company, Strategy has had time to scale and has started building its own capital stack on top of its equity. STRK, STRF, STRD, and STRC are credit-like instruments built on top of the common equity MSTR, and have become favorites of many large capital allocators. As shown in the July 2025 investor slide, these offerings have been oversubscribed, with demand led by institutions and a rising retail share, an early taste of how a crypto balance sheet inside an issuer unlocks manufacturable yield and duration.

Doesn’t this mean only MSTR should get a premium?

Currently, it’s just Strategy creating their own capital stack right now. But there are many more products besides preferred share issuances, many more flavors of risk-return, and many more avenues to create these products besides issuing them yourself. Given the strength of these initial products by Strategy, it’s not difficult to imagine a Cambrian explosion of credit instruments, derivative products, leveraged options, etc being built on top of newer DATs once they scale. This is what DATs enable and it’s only just beginning.

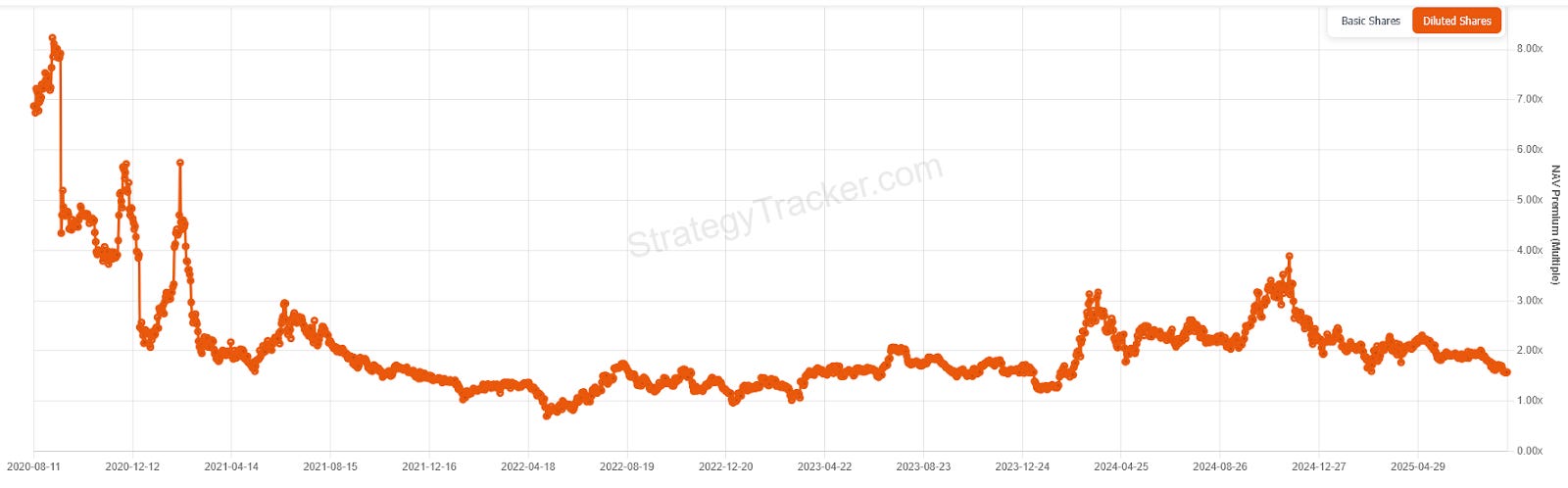

Still, one might feel that if inclusion in the capital stack is necessary for DATs to warrant mNAV premiums, then only Strategy is really large enough to warrant a large mNAV premium. This would imply that Strategy should have ever increasing mNAV premiums as it approaches a level that would make it suitable to build a capital stack on top of. However this is a misunderstanding of mNAVs. As with MSTR and other treasury companies, the historical trend is nearly always an mNAV compression as the company scales11. MSTR’s mNAV didn’t even jump when it was included in the Nasdaq100. So what gives?

This is the part that really resembles P/E multiple dynamics for tech stocks. mNAVs are how DATs grow their product (their balance sheet). Thus, higher mNAVs are a market’s signal that they want that DAT to grow fast. The larger that DAT gets, the more mNAV compresses as the upside potential goes away. And once that DAT achieves sufficient scale, its mNAV basically reaches a steady state that allows for stable growth and capital stack inclusion (arguably this is the state Strategy is in). It’s just like high-growth tech stocks with huge P/E multiples like Uber and Netflix gradually entering a steady-state phase and seeing their P/Es stabilize as they focus on earnings.

Calculating Theoretical mNAV Premiums

Such a top-down approach for justifying mNAV premiums still only establishes that NAV premiums should exist and exist higher for small and mid cap DATs. They don’ t however illustrate what the premiums ought to be.

Let’s instead approach the issue with a bottom-up approach that gives us a theoretical floor for mNAVs. We’ll take two different methods of generating asset-per-share growth to establish a theoretical mNAV floor.

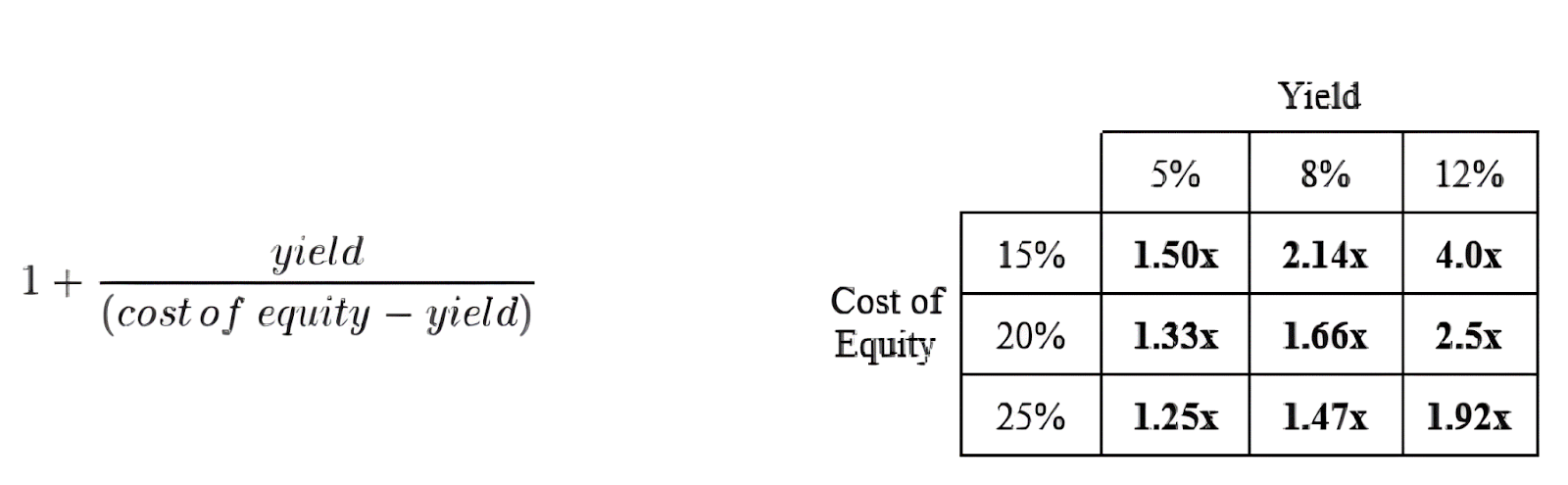

First, for companies acquiring productive assets like ETH, yield generation represents an inherent premium to NAV. If we take a company that acquires ETH and generates ~8% yield through securing the network and/or on-chain DeFi and apply a cost of equity around ~15% (similar to a high-growth tech stock), a simple Gordon-style approach returns an ~2.14x mNAV.

Second, DATs can also generate additional assets from their balance sheet by raising cheap capital and converting it into crypto. Strategy tracks the efficiency at which they do this through a metric called “BTC yield,” a KPI that represents the percentage change in the ratio between BTC count and diluted shares outstanding. Their BTC yield in 2024 was ~74%, meaning if you bought 1 share of MSTR on Jan 1, 2024, you indirectly “owned” ~74% more BTC by Dec 31, 2024.

If we assume this yield holds going forward that would imply a ~1.74x mNAV premium on MSTR’s equity purely from issuance accretion, before considering any on-chain yield. In other words, there are two drivers of premium: 1) the productivity of the asset (on-chain yield), and 2) the capital-markets accretion (BTC/ETH-per-share growth) when issuance is done above book. Both of these in conjunction create a theoretical mNAV floor at roughly 2x.

But this is only theoretical.

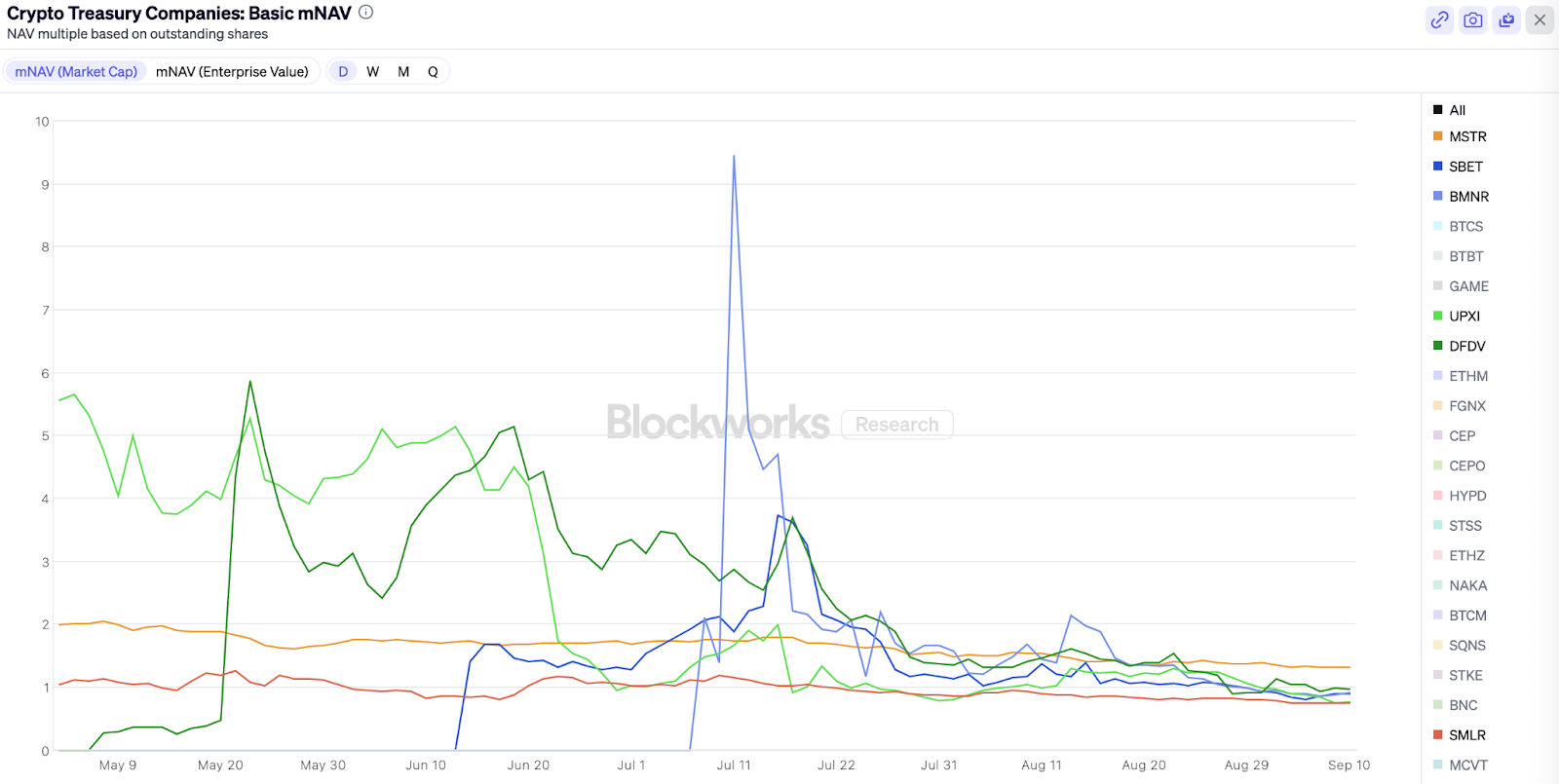

In the past couple months we have seen mNAV multiples consolidate and compress. Clearly, the market appetite for DATs has tempered and it remains to be seen what will happen going forward. At Republic, we believe mNAV cycles are cyclical in the same way P/E cycles are. When BTC and ETH make strong upward movements, market appetite will follow and mNAV multiples are likely to enter elevated zones. In less bullish markets mNAVs will compress.

Successful DATs will utilize the increased access to capital from periods of elevated mNAV efficiently and purchase crypto during less elevated periods at relative discounts. They will also differentiate themselves and warrant stronger premiums by intelligently using their balance sheets to generate yield. Those that can generate higher yields will also be able to grow their balance sheet faster.

So ultimately, the answer is quite boring: DATs will begin to look like any other frontier industry where there’s a high upside for those that know what they’re doing.

DAT premium to NAV should persist

The impact of DATs shouldn’t be understated. By putting crypto on a balance sheet, DATs open up the entire capital stack to on-chain assets: term debt, converts, preferreds, structured notes, indices, etc. Banks can underwrite it, desks can hedge it, allocators can slot it into mandates. That wasn’t possible before DATs and the floodgates are just now opening.

For DATs, their balance sheet is the product.

This brings us back to the core claim: $1 of crypto on a balance sheet can be worth more than $1 to the market when the market believes that balance sheet will eventually be the base layer of new capital markets. At a minimum, the premium stems from an issuer's capacity to increase asset-per-share exposure, and the premium can grow depending on the market’s risk appetite to scale a DAT quickly for capital markets to develop on top of it.

TLDR; Capital markets want equity-level access to a generationally undervalued asset-class, crypto. DATs provide equity-level access to crypto while also utilizing it productively. Both of these in conjunction allow DATs to issue their common stock at a premium to book, and such a premium should persist as long as there’s pent up demand from the >$100T for access to the upside of on-chain assets.

In later articles, I’ll explore the future of DATs: competition dynamics, mNAV compression, scenario analysis, and the effects DAT purchases and selloffs will have on crypto price. The transition to a fully digital economy has no precedent and new frameworks and mental models are needed. As Matt Levine would say, “well, this is finance, so everything is weird.”

About Republic Technologies

A publicly traded technology company (CSE: DOCT | FSE: 7FM0) scaling an Ethereum (ETH)-backed treasury and operating proprietary validator infrastructure.

Disclaimer: This post is for general informational purposes only and does not constitute investment advice, recommendations, or a solicitation to buy or sell any securities. It should not be used as the basis for making any investment decisions and should not be relied upon for accounting, legal, tax, or investment guidance. You are encouraged to consult your own advisors regarding legal, business, tax, or other related matters before making any investment decisions.

Certain information included here may have been obtained from third-party sources, including portfolio companies affiliated with Republic Technologies. The views expressed in this post are those of the authors and do not necessarily reflect the views of Republic Technologies or its affiliates. These opinions are subject to change without notice and may not be updated.